Worried about tax mistakes?

Complex crypto portfolio?

Optimize your crypto taxes before year-end

Turn actionable insights into smarter decisions

Withdraw crypto stress-free

<div fs-richtext-component="info-box" class="info-box warning"><div class="flex-info-card"><img src="https://assets-global.website-files.com/65098a145ece52db42b9c274/650c6f473e84badfdd6e059e_Care.svg" loading="lazy" width="64" height="64" alt="" class="icon-info-box"><div fs-richtext-component="info-box-text" class="info-box-content"><p class="color-neutral-800">The debate over reforming the Income Tax Act is in full swing: Finance Minister Lars Klingbeil's budget proposal suggests scrapping the holding period, and the Cabinet has already approved it. A concrete draft law doesn't exist yet, though. We're tracking developments for you and will update this guide as soon as there's news.</p></div></div></div>

Prefer watching this as a video instead? Right this way:

How is Crypto Taxed in Germany?

Crypto tax in Germany means: Gains and income from cryptocurrencies are generally taxable. Cryptocurrencies are considered "other assets" (§ 23 EStG) and are subject to income tax for private investors at a rate of 0–45%, depending on total personal income.

Gains from the sale or exchange of crypto are tax-free if the one-year holding period has been exceeded. Within 12 months, crypto tax applies. An exchange of coins (e.g., BTC for ETH) also counts as a sale. Example: If you bought Bitcoin on 01.01.2025, a tax-free sale is possible starting from 02.01.2026!

Furthermore, tax-free limits apply to crypto tax: Gains from private disposal transactions remain tax-free up to €999.99 per year (for previous years: €599.99). Income from staking, lending, or similar activities is tax-free up to €256 per year. If an exemption limit is exceeded, the entire amount becomes taxable.

Income Tax Rates for the Tax Year 2024 & 2025:

<figure class="block-table">

<table>

<tr>

<th>Income (2024)</th>

<th>Income (2025)</th>

<th>Steuersatz</th>

</tr>

<tr>

<td>Up to 11.784€</td>

<td>Up to 12.084€</td>

<td>0%</td>

</tr>

<tr>

<td>Up to 17.005€</td>

<td>Up to 17.430€</td>

<td>14 - 24%</td>

</tr>

<tr>

<td>Up to 66.760€</td>

<td>Up to 68.430€</td>

<td>24 - 42%</td>

</tr>

<tr>

<td>Up to 277.825€</td>

<td>Up to 277.825€</td>

<td>42%</td>

</tr>

<tr>

<td>Over 277.826€</td>

<td>Over 277.826€</td>

<td>45%</td>

</tr>

</table>

</figure>

In general, the higher the total income, the higher the average tax rate. This is referred to as a progressive tax rate.

How Do I Calculate Crypto Gains and Losses for my Tax Return? (Calculation Example)

Crypto gains are calculated as the difference between the acquisition costs and the sale price. If the result is positive, you have made a gain. If the result is negative, you have incurred a loss.

<figure class="block-table">

<table>

<tr><th>Example</th><th>Acquisition Costs</th><th>Sale Price</th><th>Result</th><th>Tax Status</th></tr>

<tr><td>Calculation Example 1</td><td>€1,400</td><td>€2,200</td><td>+€800 Gain</td><td>Taxable if holding period < 1 year and exemption limit exceeded</td></tr>

<tr><td>Calculation Example 2</td><td>€1,400</td><td>€1,200</td><td>-€200 Loss</td><td></td></tr>

</table>

</figure>

There are various methods for determining the acquisition costs of cryptocurrencies, known as cost flow assumptions. These are relevant if you purchased coins at different times and prices.

In Germany, the FiFo method (First-In, First-Out) is typically used to calculate crypto taxes. Under this method, the coins purchased first are considered to be the first ones sold.

Keep more money in your account by legally optimizing your crypto taxes. You can claim crypto losses for tax purposes and offset them against gains – this is known as Tax Loss Harvesting. Unused losses can be carried forward indefinitely to future years or carried back to the immediately preceding tax year.

<div fs-richtext-component="info-box" class="info-box protip"><div class="flex-info-card"><img src="https://assets-global.website-files.com/65098a145ece52db42b9c274/650c6f4b151815fb0be48cec_Lightning.svg" loading="lazy" width="64" height="64" alt="" class="icon-info-box"><div fs-richtext-component="info-box-text" class="info-box-content"><p class="color-neutral-800">Tools like the Crypto Tax Optimizer included in Blockpit Plus help you discover hidden optimization opportunities in your portfolio and save taxes efficiently. Our users save an average of €2,395.</p></div></div></div>

How Do I Calculate Crypto Income for Tax Returns?

Crypto income (e.g., from staking, lending, mining, or bounties) is taxed in Germany at the time of receipt. The market value in Euros on the day of receipt is the decisive factor. This amount is classified as other income under § 22 No. 3 EStG and is subject to your personal income tax rate (0–45%).

Additionally, an annual exemption limit of €256 applies to other services. If this limit is exceeded, the entire amount becomes taxable.

If you sell the received coins later within one year and at a profit, additional crypto tax applies as part of a private disposal transaction (§ 23 EStG).

<div fs-richtext-component="info-box" class="info-box definition"><div class="flex-info-card"><img src="https://assets-global.website-files.com/65098a145ece52db42b9c274/650c6f473db41a468e9c5dc5_Bookmark.svg" loading="lazy" width="64" height="64" alt="" class="icon-info-box"><div fs-richtext-component="info-box-text" class="info-box-content"><p class="color-neutral-800">Exclusive - Our experience from 1,000,000+ tax reports: Staking is increasingly becoming the standard: The share of German Blockpit users with staking increased from 33% (2024) to around 40% (2025) – while the average reward in the same period fell from €218 to about €100 per year.</p></div></div></div>

How Do I File a Tax Return for Cryptocurrencies?

Filing your cryptocurrency tax return is part of your annual income tax return submitted to your local tax office. You can submit the income tax return using the ESt 1 A form, either on paper with official forms or electronically via the Elster Portal.

Please note: Even if you are not normally required to submit a tax return, taxable gains and income from cryptocurrencies must be reported to the tax office.

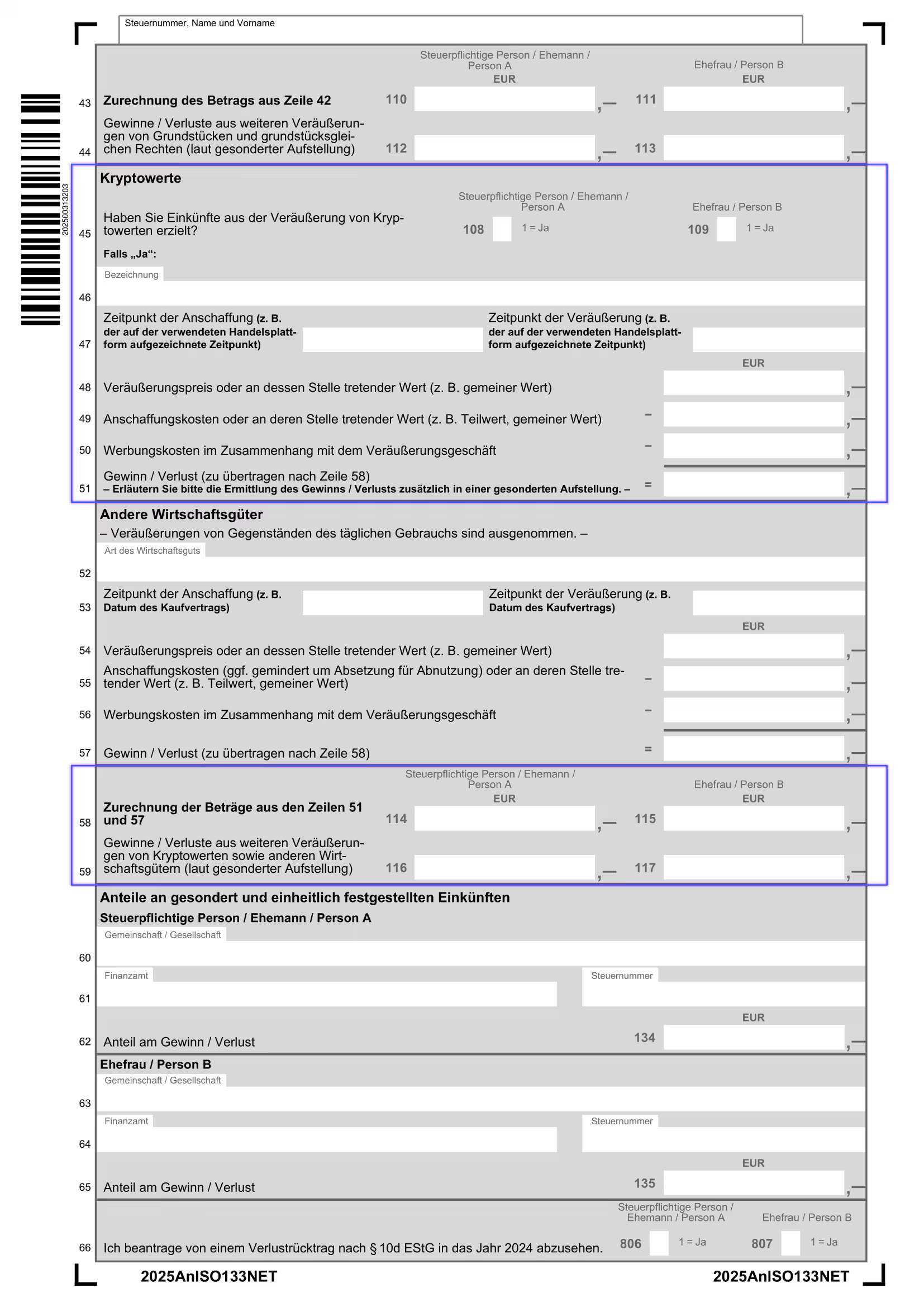

For the 2025 tax year, there are specific sections in the Anlage SO form on page 2 dedicated to "Kryptowerte".

Line 45: Enter 1 in box 108 if you earned income from the sale of cryptocurrencies. Box 109 is for spouses.

Line 46: Enter “cryptocurrencies” or the specific name of a cryptocurrency. If you carried out multiple different transactions, you can refer to the Blockpit tax report, which you can submit together with your tax return.

Line 47: Enter the date of acquisition and disposal. If there were multiple transactions, you can also simply enter the full period from 01/01/2023 to 31/12/2023.

Line 48: Enter the total disposal proceeds of all cryptocurrencies sold.

Line 49: Enter the total acquisition costs of all cryptocurrencies sold.

Line 50: Enter all expenses related to the purchase or sale, such as transaction fees.

Blockpit automatically deducts transaction fees from the gain, so they should not be entered again here.

Line 51: Subtract the acquisition costs (line 49) and expenses (line 50) from the disposal proceeds (line 48). The result is your gain or loss.

Line 58: Enter the amount from line 51 in box 114. Box 115 is for spouses.

Line 59: Gains or losses from other disposals, such as the sale of art or gold, must be entered in box 116. Box 117 is for spouses.

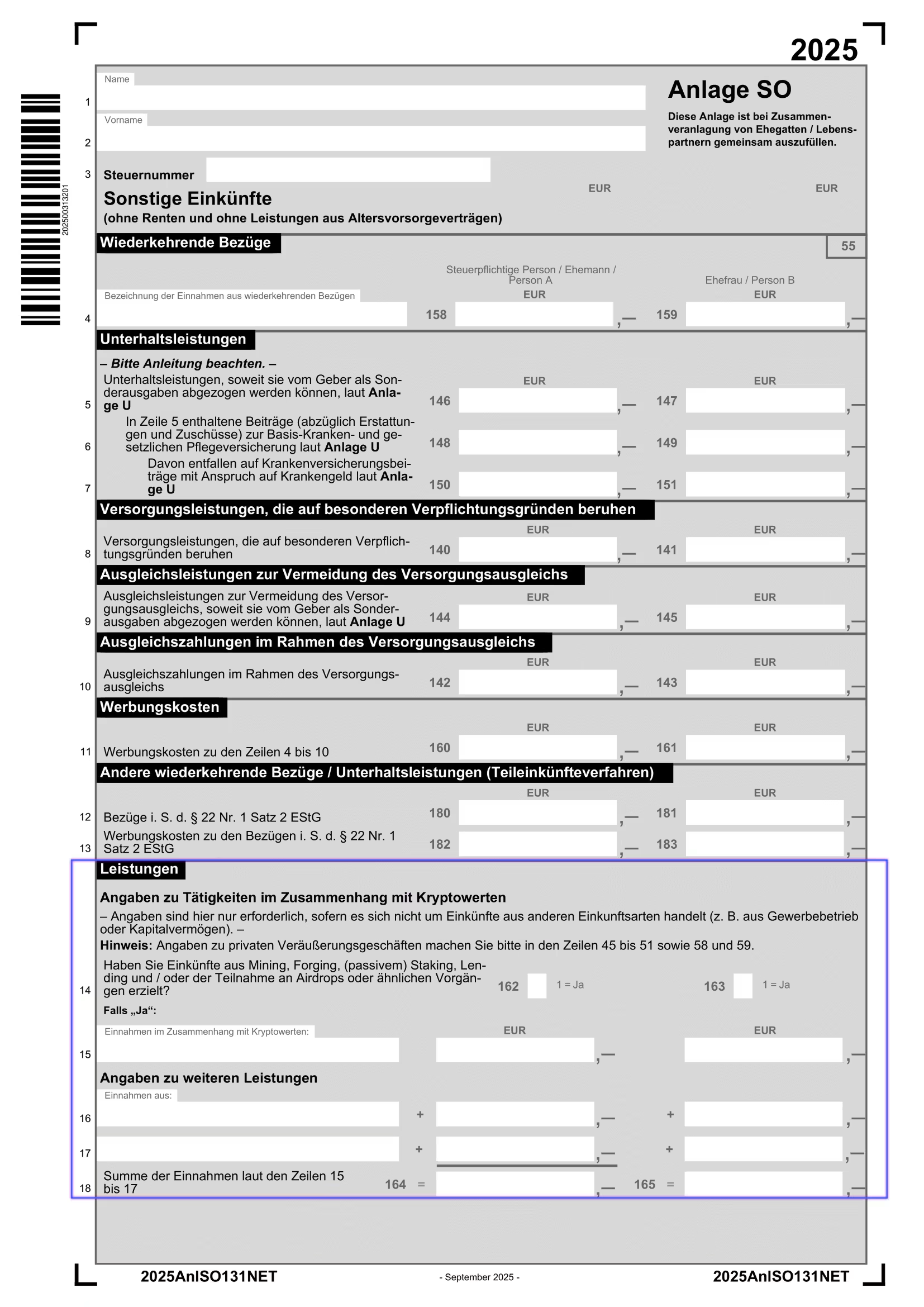

Entering crypto income in the tax return

Crypto income generated from staking, mining, lending, airdrops, or other activities must also be declared in Form ESt 1 A, in Annex SO. On page 1 of Annex SO, you will find the section “Leistungen - Angaben zu Tätigkeiten im Zusammenhang mit Kryptowerten”.

Line 14: Enter a 1 in box 162 if you earned income from cryptocurrencies.

Line 15: On the left, specify the type of income and enter the amount on the right. If you have multiple types of crypto income, you can refer to your Blockpit tax report here and submit it as an attachment. Blockpit automatically totals all income in line 15.

Lines 16 + 17: Enter additional types of income here, if applicable.

Line 18: Add up all amounts from lines 15, 16, and 17.

Line 19: Enter any deductible expenses related to earning this income.

Line 20: Enter the calculated income (line 18 minus line 19).

Crypto derivatives in the tax return

If you earned income from crypto derivatives (futures), these must be declared in Annex KAP for investment income.

Lines 19 and 20: Enter profits from derivative transactions here.

Line 22: Enter losses from derivative transactions here.

When Is the Tax Return Due?

The deadline for the 2025 tax return is July 31, 2026. This applies to both online and paper submissions.

If you have your tax return prepared by tax advisors, the deadline extends to March 1, 2027.

Tax advisors also appreciate Blockpit's tax reports! They save a lot of work—and save you money!

When Do Crypto Taxes Apply?

<figure class="block-table">

<table>

<tr><th>Transaction</th><th>Tax</th><th>Brief Info</th></tr>

<tr><td>Sale for Fiat</td><td>Income Tax 0–45%</td><td>Taxable if held < 1 year + > €999.99 gain/year (exemption limit)</td></tr>

<tr><td>Paying with Crypto</td><td>Income Tax 0–45%</td><td>Treated as a sale at market value</td></tr>

<tr><td>Crypto Swap (BTC→ETH)</td><td>Income Tax 0–45%</td><td>Taxable if held < 1 year + > €999.99 gain/year (exemption limit)</td></tr>

<tr><td>Stablecoin Trading</td><td>Income Tax 0–45%</td><td>No special rules; same as regular coins</td></tr>

<tr><td>Airdrop</td><td>€0 at receipt</td><td>Acquisition cost €0; sale within < 1 year is taxable</td></tr>

<tr><td>BEST Rewards</td><td>€0 at receipt</td><td>Acquisition cost €0; sale within < 1 year is taxable</td></tr>

<tr><td>Bounties</td><td>0–45% at receipt</td><td>Consideration for service → immediately taxable; sale within < 1 year also taxable</td></tr>

<tr><td>NFTs</td><td>Income Tax 0–45%</td><td>Same as crypto swap; > 1 year tax-free</td></tr>

<tr><td>DeFi Rewards</td><td>Income Tax 0–45%</td><td>Receipt is taxable; €256 exemption limit; sale < 1 year taxable</td></tr>

<tr><td>Staking</td><td>Income Tax 0–45%</td><td>Receipt is taxable; €256 exemption limit; sale < 1 year taxable</td></tr>

<tr><td>Lending</td><td>Income Tax 0–45%</td><td>Receipt is taxable; €256 exemption limit; sale < 1 year taxable</td></tr>

<tr><td>Mining (private)</td><td>Income Tax 0–45%</td><td>Receipt is taxable; €256 exemption limit; sale < 1 year taxable</td></tr>

<tr><td>ICO / IEO</td><td>Income Tax 0–45%</td><td>Taxable if held < 1 year + > €999.99 gain/year (exemption limit)</td></tr>

<tr><td>Margin Trading</td><td>Capital Gains Tax 25%</td><td>Derivative transaction; no holding period; if crypto is delivered, potentially private disposal transaction</td></tr>

<tr><td>Futures</td><td>Capital Gains Tax 25%</td><td>Derivative transaction; no holding period; if crypto is delivered, potentially private disposal transaction</td></tr>

<tr><td>Wrapping</td><td>Income Tax 0–45%</td><td>According to prevailing view: tax-relevant if profit is made</td></tr>

</table>

</figure>

What is Tax-Free?

<figure class="block-table">

<table>

<tr><th>Transaction</th><th>Tax Status</th><th>Brief Info</th></tr>

<tr><td>Purchase with Fiat (e.g., EUR)</td><td>Tax-free</td><td>Mere acquisition – no taxable event</td></tr>

<tr><td>Transfers between own Wallets/Exchanges</td><td>Tax-free</td><td>Movement between own accounts only; ensure clear documentation</td></tr>

<tr><td>Gifts (up to €20,000/year)</td><td>Tax-free</td><td>Spouses: €500,000; 10-year period; holding period transfers to the recipient</td></tr>

<tr><td>Donations</td><td>Tax-free</td><td>No taxation</td></tr>

<tr><td>True Crypto Swap (Project-internal)</td><td>Tax-neutral</td><td>Not a taxable exchange as defined by § 23 EStG</td></tr>

<tr><td>Hard/Soft Fork</td><td>Tax-free</td><td>Original asset remains unchanged; new coins usually have €0 acquisition cost</td></tr>

<tr><td>Exchange/Gas Fees</td><td>Tax-deductible</td><td>Can be claimed as expenses and offset against gains</td></tr>

<tr><td>Cashback (Crypto)</td><td>Potentially tax-free</td><td>Treated as a discount; usually not relevant for income tax; legally debated; potentially "other income"</td></tr>

</table>

</figure>

Stay on the Safe Side with Blockpit

One platform. Two paths. More crypto tax confidence – do it yourself or let Blockpit Experts prepare your report.

- Start for free: Registration with email only – no payment details required.

- Document everything seamlessly: Record your crypto transactions in full, including retroactively for previous years. Don't wait for mail from the tax office – take precautions now.

- Optimize taxes: Take advantage of legal optimization opportunities and save an average of up to €2,395 per year!

- Or hand it off: Let certified Blockpit Experts handle setup and report preparation. You stay involved only where it counts.

Crypto Tax FAQ

Does the Tax Office Know I Own Cryptocurrencies?

Cryptocurrency trading isn't as anonymous as one might think. Authorities can track crypto transactions and link them to personal data, especially through legal pressure on crypto exchanges. New regulations like DAC8 and MiCA are further aimed at combating tax evasion involving cryptocurrencies.

Do I Need to Pay Taxes on Crypto Profits from Years Ago?

Yes. It's advisable to keep records of your cryptocurrency transactions for the past 10 years as there's a chance you might be audited. In the volatile crypto space, amounts can quickly add up. Significant tax evasion occurs when the evaded tax exceeds €50,000.

Are Cryptocurrencies Taxed Like Stocks?

No, cryptocurrencies are not taxed like stocks. Profits from stock trading are considered capital gains and are taxed at a flat rate of 25% in Germany (capital gains tax). Cryptocurrencies, however, are classified as "private economic goods." Thus, their trading profits are subject to income tax, not capital gains tax.

Can I Pay Taxes with Cryptocurrencies?

No, that is not currently possible in Germany.

What should be considered when inheriting or bequeathing crypto assets?

To ensure your digital legacy remains accessible and doesn't become a financial burden, three points are essential:

- Secure Access: Establish a clear access strategy (e.g., a digital legacy folder) early on so that heirs are capable of taking action and do not lose access to wallets and private keys.

- Manage Tax Risks: Inheritance tax is calculated based on the market value on the day of death. If crypto prices drop sharply after that date, the tax liability remains fixed, which can lead to significant liquidity issues if the tokens are worth less than the tax owed.

- Legal & Documentation: Use a combination of a will, trans-mortal powers of attorney, and a complete transaction history (e.g., via Blockpit) to ensure the digital estate is managed legally, efficiently, and with full transparency for tax authorities.

In Which Countries are Cryptocurrencies Tax-Free?

Countries like Portugal, Singapore, Malta, and Switzerland are considered very crypto-friendly for individuals.

Where Can I Learn More About Cryptocurrencies and Taxes?

We have published a variety of guides on various crypto tax topics in Germany, all available here: Blockpit Crypto Tax Guides.

Our crypto experts write detailed articles and useful guides on the Blockpit Blog to help you understand crypto, make better investment decisions, and find the best crypto tools.

In the Blockpit Community, you can engage with other users and tax experts on all topics related to cryptocurrencies, taxes, and regulations. Updates from the Federal Ministry of Finance (BMF) and the Federal Central Tax Office (BZSt) on current changes are also available.

Frequently Asked Questions about Crypto Tax in Germany

Is crypto tax-free after one year in Germany?

Yes. Under § 23 EStG, cryptocurrency held for more than 12 months is completely tax-free upon disposal — regardless of the gain amount. This one-year Haltefrist (holding period) is one of the most favourable provisions for long-term crypto investors in Europe.

What is the €1,000 Freigrenze for crypto in Germany?

The €1,000 Freigrenze (tax-free allowance) applies to all private disposal transactions including crypto sold within the one-year holding period. If your total gains from such transactions stay below €1,000 in a tax year, no tax is due. Importantly, this is a Freigrenze (threshold), not a Freibetrag — if you exceed €1,000, the full amount becomes taxable.

Are crypto-to-crypto trades taxable in Germany?

Yes. In Germany, exchanging one cryptocurrency for another (e.g., Bitcoin to Ethereum) is a taxable disposal event under § 23 EStG. The gain is calculated based on the original purchase price and the market value at the time of the swap. The one-year holding period and €1,000 Freigrenze both apply.

Helpful Links

05/2026: Article reviewed and updated for 2026.

April 2026: Content Update

January 2026: Update for 2026

July 2024: Complete revision; new structure, texts and images

February 2024: Update for 2024 / New tax forms